1031 Exchange Timeline: Every Deadline You Need

A 1031 exchange can defer capital gains taxes indefinitely, but only if you hit every deadline, in order, without exception. Miss any one of them, and the IRS will treat your transaction as a taxable sale.

This guide walks through the entire 1031 exchange timeline: every deadline, every identification rule, the special situations that can extend or compress your window, and the timing traps that catch even experienced investors off guard.

The 1031 Exchange Timeline at a Glance

The three deadlines, the actions each one requires, and how unevenly the time is distributed between them.

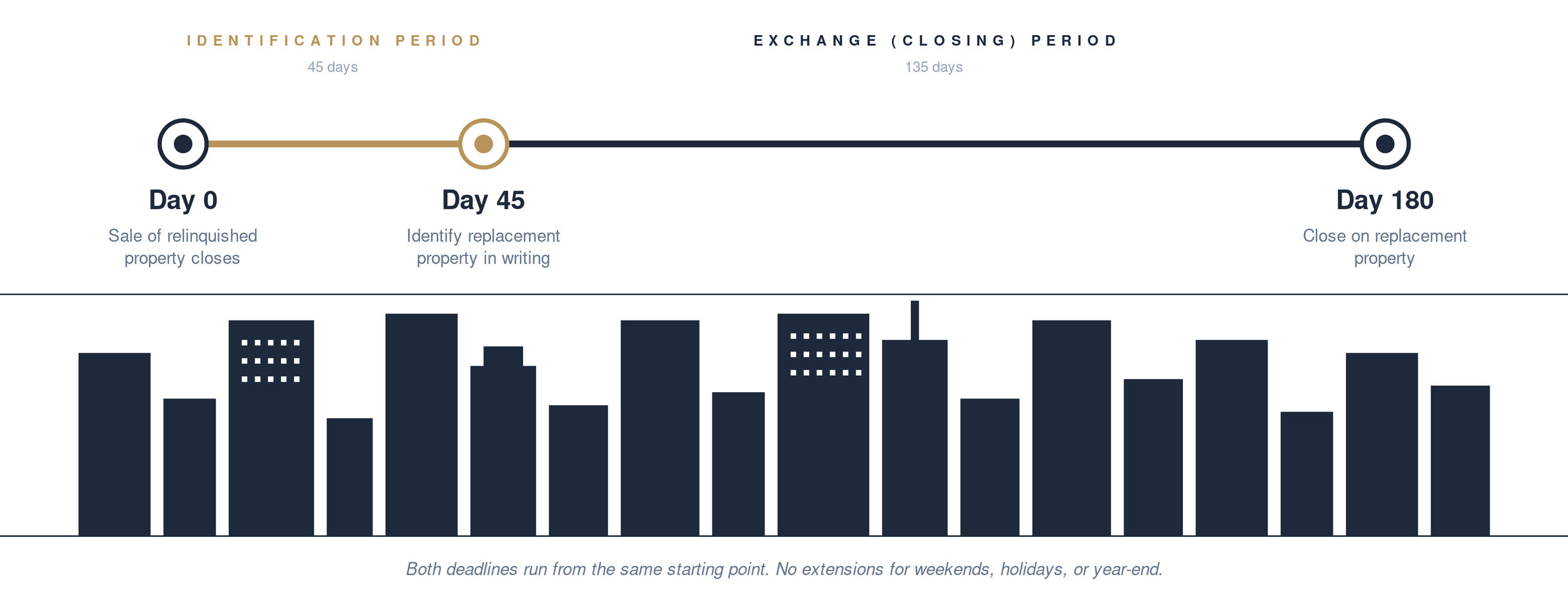

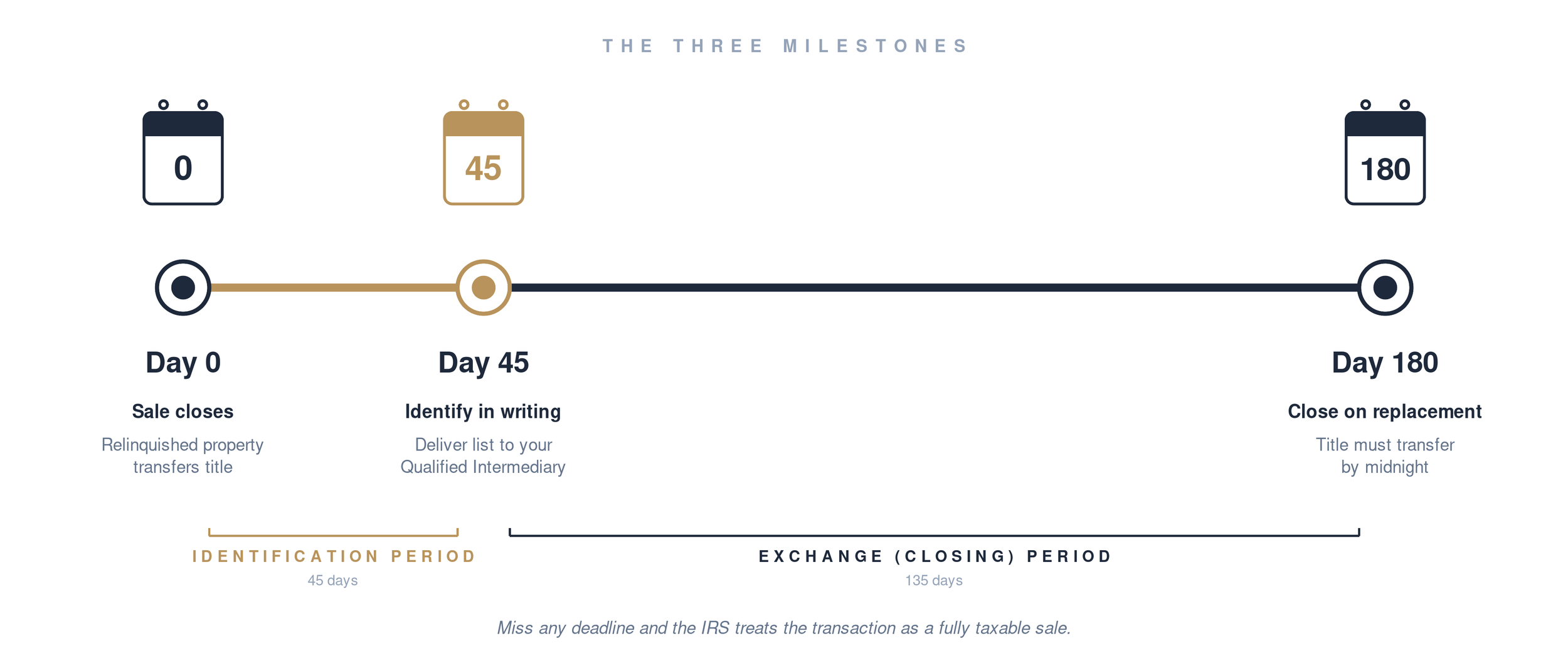

A standard 1031 exchange has two hard deadlines, both triggered by the same event:

Day 0: You close on the sale of your relinquished property.

Day 45: You must identify replacement property in writing to your Qualified Intermediary.

Day 180: You must close on the purchase of your identified replacement property.

Both deadlines run concurrently from the same starting point. The 180-day clock does not reset or extend when you identify your replacement property; it ends on the 180th day from your original sale, period.

There is no extension for weekends, holidays, or year-end. If day 45 falls on a Sunday, your identification is still due on Sunday. The only exception is presidentially declared disaster relief, discussed below.

Day 0: The Sale of Your Relinquished Property

The exchange clock starts the day the relinquished property's sale closes, defined as the day title transfers, which is typically the recorded deed date.

A few critical points about day 0:

Sale proceeds cannot touch your hands. For the exchange to qualify under Section 1031, the proceeds from the sale must go directly to a Qualified Intermediary (QI), not to you, your spouse, your bank account, or any related party. If you take constructive receipt of the funds at any point, the exchange is dead.

The QI must be in place before closing. You cannot retroactively assign sale proceeds to a QI after closing. The QI agreement must be signed and recorded before the relinquished property sale closes.

Choose your QI carefully. Qualified Intermediaries are not regulated at the federal level (a handful of states regulate them), and a QI bankruptcy or fraud event can permanently destroy an exchange. Use a QI with substantial assets, fidelity bonds, and a long operating history.

Day 1 to Day 45: The Identification Period

From the day after closing on your relinquished property, you have exactly 45 calendar days to identify your replacement property (or properties) in writing.

Identification must be:

In writing. Verbal identification does not count.

Signed by the exchanger (you).

Delivered to the Qualified Intermediary (not your attorney, not your accountant, not the seller).

Specific. Replacement property must be described unambiguously, typically by street address or legal description.

Delivered on or before midnight of day 45.

You may revoke and replace identifications during the 45-day window, but once day 45 passes, your identification is locked. You cannot add, change, or substitute.

The Three Identification Rules

The three IRS rules for identifying replacement property. You must satisfy at least one.

The IRS allows you to identify replacement property under any one of three rules. You must satisfy at least one.

The 3-Property Rule. You can identify up to three properties of any value. This is the most commonly used rule and gives most investors enough flexibility.

The 200% Rule. You can identify more than three properties, provided the aggregate fair market value of all identified properties does not exceed 200% of the value of your relinquished property. This rule is useful for investors planning to acquire multiple smaller properties.

The 95% Rule. You can identify any number of properties of any aggregate value, provided you actually acquire at least 95% (by value) of all identified properties within the 180-day window. This rule is rarely used because failing to close on even one property can blow the entire exchange.

For most investors using DSTs, the 3-Property Rule is sufficient: they identify one or two primary candidates and a DST as a backup.

Day 46 to Day 180: The Exchange (Closing) Period

You have until midnight of the 180th day from the relinquished property sale to close on your identified replacement property.

A few critical clarifications:

The 180-day clock runs from day 0, not day 45. If you wait until day 45 to identify, you still have only the remaining 135 days to close, not a fresh 180.

You can only acquire identified property. You cannot decide on day 100 to buy a property you did not identify by day 45. Whatever you close on must be on your identification list.

The 180-day deadline OR your tax return due date, whichever is earlier. This is the trap that catches investors who sell late in the calendar year. If you sell your relinquished property in November or December, your tax return due date (April 15) may arrive before your 180-day window closes. To preserve the full 180 days, you must file a tax extension (Form 4868 for individuals).

Closing means closing. The IRS measures completion as the date title transfers on your replacement property, not the date you sign a contract or place an offer.

What Happens If You Miss a Deadline?

If you miss the 45-day identification deadline or the 180-day closing deadline, the IRS treats your transaction as a fully taxable sale. The consequences:

Capital gains tax on the appreciation since you acquired the relinquished property

Depreciation recapture at a rate of up to 25% on all depreciation taken during your ownership

Net investment income tax of 3.8% if applicable

State income tax in most states

For a long-held investment property, the combined tax bill can easily reach 30% to 40% of the gain. There is no grace period and no retroactive relief except in the disaster-relief situations below.

Special Timing Situations

A few situations alter or extend the standard 1031 timeline.

Presidentially Declared Disaster Relief

When a federally declared disaster affects an area where the exchange is happening (either where the property is located or where the exchanger resides), the IRS can issue notices extending the 45-day and 180-day deadlines. These extensions are not automatic. Check IRS guidance after any major disaster to confirm whether your exchange qualifies.

Reverse 1031 Exchanges

In a reverse 1031 exchange, you acquire the replacement property before selling the relinquished property. The same 45-day and 180-day timeline applies, but it runs from the date the replacement property is "parked" with an Exchange Accommodation Titleholder (EAT) rather than from a sale closing.

Within 45 days, you must identify which property (or properties) you intend to sell. Within 180 days, the relinquished property must be sold and the parked replacement property must be transferred to you.

Reverse exchanges are significantly more complex and expensive than forward exchanges and are typically used only when timing forces the acquisition before the sale (for example, when the replacement property is uniquely desirable and the seller will not wait).

Improvement (Build-to-Suit) Exchanges

In an improvement exchange, exchange proceeds are used to fund construction or improvements on the replacement property within the 180-day window. The improved property must be received by the exchanger by day 180, with all improvements completed by that date for the cost to count toward the exchange value.

Improvement exchanges create real timing risk: any construction delay past day 180 can invalidate the value of unfinished improvements.

Year-End and Tax Return Timing

For sales that close in the fourth quarter, the tax return due date (typically April 15 of the following year) often arrives before the 180-day window expires. To preserve the full 180 days, file a tax extension. Without an extension, your exchange period is effectively shortened to whatever falls between the sale closing and April 15.

Tips for Staying on Schedule

A few practical disciplines that experienced exchangers use:

Start identifying replacement property before you list the relinquished property. The 45-day window is much shorter than it sounds, especially in a tight market. Investors who wait until after closing to start searching almost always end up under pressure.

Build a backup identification list. Even if you have a primary deal under contract by day 45, identify a DST or two as a backup. If the primary deal collapses on day 75, you cannot add a new property to your list.

Coordinate with your CPA early. Your CPA should know about the exchange before the relinquished property closes, not after. Late-year sales especially require tax-extension planning.

Choose a QI you've verified. Confirm bonding, errors-and-omissions insurance, and segregated client accounts. The cheapest QI is rarely the right one.

Calendar every deadline immediately. On day 0, calendar day 45 and day 180 (and the tax return due date). Set reminders at day 30, day 40, day 44, day 150, and day 170.

Frequently Asked Questions

Do the 45-day and 180-day deadlines fall on calendar days or business days? Calendar days. Weekends and holidays count. There is no extension if a deadline falls on a non-business day.

Can I extend a 1031 exchange? Generally, no. The only extensions are those granted by IRS notice in connection with a federally declared disaster.

What if my replacement property closes on day 181? The exchange fails. The transaction becomes a fully taxable sale.

Can I change my identified properties after day 45? No. After midnight of day 45, your identification is permanently locked.

What happens if I identify three properties but only buy one? That's fine, provided the property you acquire is one of the three you identified and you close by day 180. There is no requirement to acquire all identified properties under the 3-Property Rule.

Does the 180-day deadline reset if I identify a different property? No. Both deadlines run from the relinquished property sale closing, not from any subsequent event.

What's the latest I can sell my relinquished property and still complete the exchange in the same tax year? Roughly July 4, about 180 days before year-end. Sales after that date will require a tax extension to preserve the full exchange window.

The Bottom Line

The 1031 exchange timeline is unforgiving: 45 days to identify, 180 days to close, no extensions except in declared disasters, and no grace period for honest mistakes. Investors who treat the timeline as flexible end up paying tax they could have deferred.

The investors who execute exchanges cleanly do three things differently. They start the search before they sell. They identify a DST or other backup option by day 45. And they coordinate with their CPA and Qualified Intermediary from day one, not from day 44.

Considering a 1031 exchange?Talk to a Specialist about your timeline, your replacement options, and whether a DST might fit your situation. You can also try our 1031 Calculator to estimate your potential tax savings.