Delaware Statutory Trusts, Explained for 1031 Investors

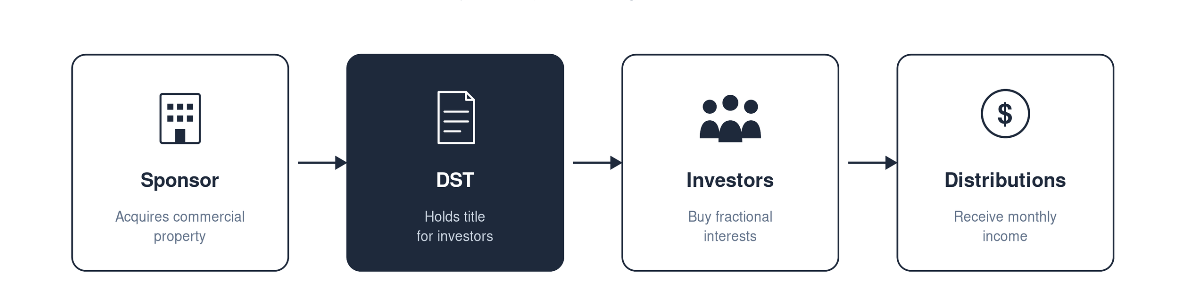

How a DST investment works: from sponsor acquisition through investor distributions.

For real estate investors facing the end of a 1031 exchange's 45-day identification window, or for property owners simply tired of being landlords, Delaware Statutory Trusts (DSTs) have become one of the most widely used replacement property structures in commercial real estate.

But "DST" is also one of the most misunderstood acronyms in the 1031 exchange world. This guide explains what a Delaware Statutory Trust is, how it qualifies for 1031 exchange treatment, how a DST investment actually works, and the benefits and risks every investor and tax advisor should understand before committing capital.

What Is a Delaware Statutory Trust (DST)?

A Delaware Statutory Trust is a legally recognized real estate investment vehicle that holds title to one or more income-producing properties on behalf of multiple investors. Each investor owns a fractional beneficial interest in the trust, and through that interest, a proportional share of the underlying real estate and its income.

DSTs are formed under the Delaware Statutory Trust Act, originally enacted in 1988 as the Delaware Business Trust Act and renamed in 2002. The act provides a flexible legal framework that gives DSTs strong contractual freedom and clear separation between the trust entity and its beneficiaries. While the trust is formed in Delaware, the real estate it holds can be located anywhere in the United States.

The key feature that matters to 1031 exchange investors: the IRS treats a beneficial interest in a properly structured DST as a direct interest in real estate for federal tax purposes. That means a DST interest qualifies as like-kind replacement property in a 1031 exchange.

How DSTs Qualify for 1031 Exchanges: IRS Revenue Ruling 2004-86

DSTs were not always eligible for 1031 exchange use. The structure was opened up by a single IRS ruling: Revenue Ruling 2004-86, issued in August 2004.

That ruling established that a beneficial interest in a properly structured DST is treated as a direct interest in real property under Section 1031 of the Internal Revenue Code. Before Revenue Ruling 2004-86, most fractional ownership in 1031 exchanges happened through Tenant-in-Common (TIC) structures, which carried significant administrative and lender complications.

However, Revenue Ruling 2004-86 also imposed strict limitations on what a DST can and cannot do during the holding period. Industry practitioners refer to these limits as "the seven deadly sins" of DSTs:

The trust cannot accept additional capital contributions from current or new investors once the offering closes.

The trustee cannot renegotiate the terms of existing loans or borrow new funds (with limited exceptions).

The trustee cannot reinvest sale proceeds from the property.

Capital expenditures are limited to normal repair, maintenance, and minor non-structural improvements.

Cash held between distributions can only be invested in short-term debt obligations.

All cash other than necessary reserves must be distributed to investors on a regular basis.

The trustee cannot enter into new leases or renegotiate current leases (except in cases of tenant bankruptcy or insolvency).

These restrictions exist to preserve the trust's tax classification. They also explain why DSTs are typically structured around stable, long-term lease arrangements. There is no flexibility to actively manage a property mid-stream.

How a DST Investment Actually Works

How a DST investment works: from sponsor acquisition through investor distributions.

The mechanics of a DST investment look very different from owning a rental property directly. Here's the typical sequence:

The sponsor identifies and acquires the property. A DST sponsor (usually a real estate firm with operational, acquisition, and securities expertise) identifies a commercial property such as a net-leased retail building, industrial facility, medical office, or multifamily complex. The sponsor arranges financing and acquires the asset.

The sponsor structures the offering. The sponsor places the property into the DST and files a private placement offering (typically under Regulation D, Rule 506(b) or 506(c) of the Securities Act). The offering is open only to accredited investors.

Investors purchase beneficial interests. Accredited investors, often coming from a 1031 exchange, purchase fractional interests. Minimum investments commonly range from $25,000 to $100,000, though this varies by sponsor.

The sponsor manages the property. Throughout the hold period (usually 5 to 10 years), the sponsor or its affiliated property manager handles all leasing, tenant relations, maintenance, and reporting. Investors receive monthly or quarterly distributions and annual K-1 (or 1099) tax reporting.

The sponsor sells the property. At the end of the hold period, the sponsor sells the asset and distributes the net proceeds to investors. Investors then face a choice: pay tax on the gain, or roll their proceeds into another 1031 exchange (often into another DST).

Benefits of DSTs for 1031 Exchange Investors

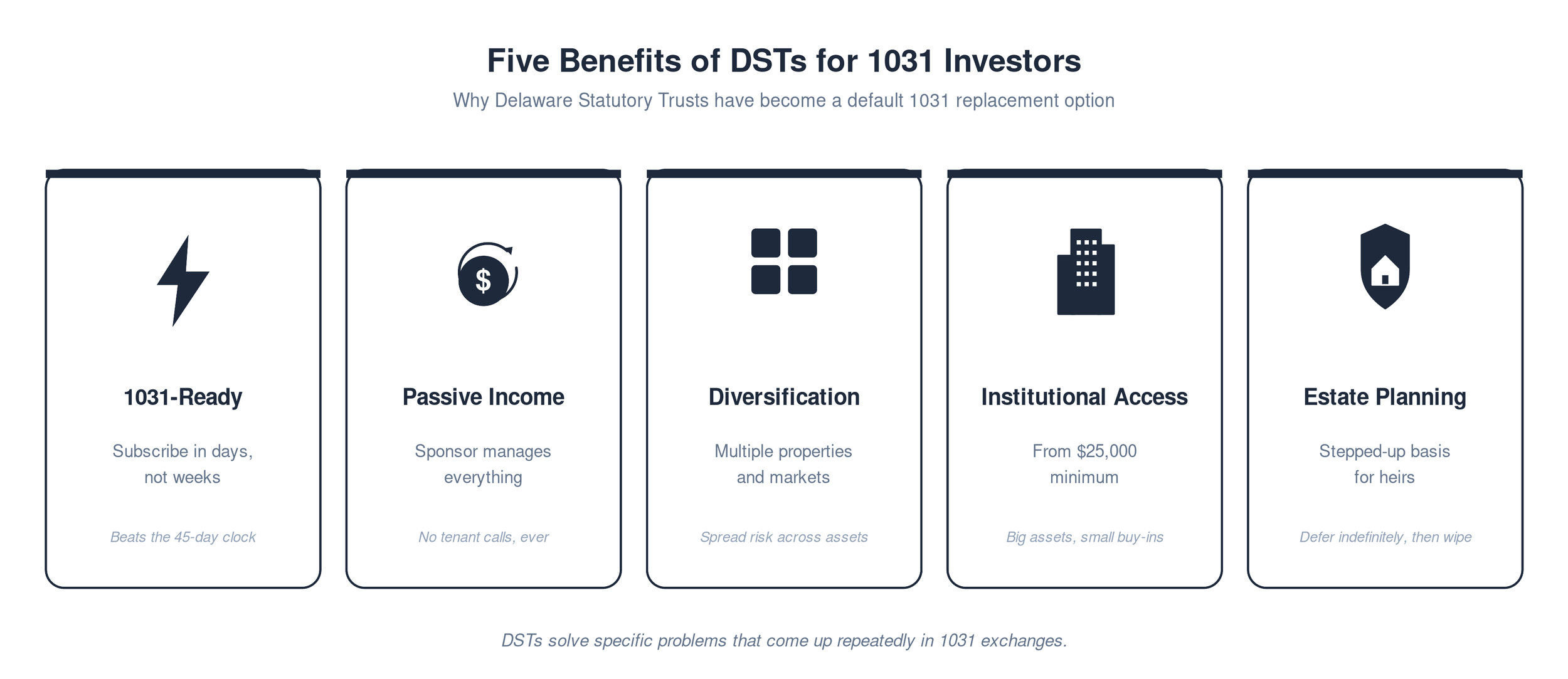

The five benefits that make DSTs a fit for many 1031 exchange investors.

DSTs solve a number of specific problems that come up repeatedly in 1031 exchanges and in the lives of long-term property owners.

Pre-packaged 1031 replacement property. The single biggest reason investors use DSTs is timing. A 1031 exchange gives you 45 days to identify replacement property and 180 days to close. A DST offering can typically be subscribed in days, not weeks, which is critical when other deals fall through near the deadline.

True passive income. DSTs are managed entirely by the sponsor. There are no tenant calls, no broken HVAC systems, no leasing decisions. Investors receive distributions without operational responsibility, a meaningful change for those who have spent years actively managing rental property.

Diversification across properties, tenants, and geography. Because minimum investments are relatively low, an investor can spread the proceeds of a single property sale across multiple DSTs: perhaps one in industrial, one in multifamily, and one in net-leased retail, across different markets. This is much harder to do with direct ownership.

Institutional-grade assets at lower entry points. DSTs typically hold properties valued in the tens of millions of dollars, assets most individual investors could never access directly. A $100,000 investment can buy a fractional interest in a property that would otherwise require $20 million of equity to own outright.

Estate planning advantages. DST interests pass to heirs with a stepped-up cost basis, the same as direct real estate. This means that all the deferred capital gain across multiple 1031 exchanges can ultimately be eliminated at the original owner's death. It is a powerful, often-underused estate strategy.

Backup identification. Even investors who plan to acquire a direct replacement property often identify a DST as a backup in their 45-day identification. If the primary deal falls through, the DST provides a safety net that preserves the exchange's tax-deferred status.

Risks and Limitations of DSTs

DSTs are not the right answer for every investor, and the structure carries real risks that any serious due diligence process needs to address.

Illiquidity. A DST interest is not publicly traded. There is no secondary market in any meaningful sense. Investors should expect to hold for the full 5-to-10-year period, and possibly longer if market conditions delay the sponsor's exit.

No control or voting rights. Investors have essentially no say in how the property is managed, when it is sold, or how distributions are structured. The sponsor's decisions are binding.

Sponsor risk. The single most important variable in DST investing is the sponsor. A sponsor with a poor track record, weak underwriting discipline, misaligned fee structures, or insufficient operational depth can turn a sound property into a poor investment.

Fee layers. DST offerings typically include acquisition fees, asset management fees, disposition fees, and load fees paid to the broker-dealer. These can total 8% to 15% of the offering amount and are disclosed in the Private Placement Memorandum (PPM).

Property-level risk. As with any real estate investment, the underlying property can underperform. Tenants default, market rents softe

isn, capital improvements become necessary. The DST's inability to refinance, renegotiate leases, or reinvest sale proceeds (per the seven deadly sins) limits the sponsor's ability to respond.

Tax-cost exit. When the DST eventually sells, investors face the same decision they faced at the beginning: pay the deferred tax now, or roll into another 1031 exchange. Investors who want full liquidity at exit need to plan for the tax consequence.

Who Should Consider a DST?

DSTs are not universally appropriate. They tend to work well for:

Tired landlords who want to preserve the tax-deferred status of their real estate equity but are ready to step away from active property management.

Time-pressed 1031 exchangers who have lost a deal near the identification deadline and need a reliable backup that can close quickly.

Estate planners who want to consolidate fragmented direct holdings into a more manageable position that will receive a stepped-up basis at death.

Diversification-focused investors who want to spread the proceeds of a large property sale across multiple geographies, asset classes, and tenants without managing each one.

Accredited investors only. Every DST offering is restricted to accredited investors, those meeting SEC income or net worth thresholds. This is a regulatory requirement, not a sponsor preference.

DSTs are typically less appropriate for investors who need liquidity in the near term, who want active control over their real estate decisions, or who cannot tolerate the illiquidity profile of a 7-to-10-year hold.

DST vs. Other 1031 Replacement Options

DSTs are one of several structures eligible for 1031 exchange use. A brief comparison:

Direct ownership. Total control, full responsibility, full upside (and downside). Best for investors who want to remain actively involved.

Tenant-in-Common (TIC). A pre-DST fractional ownership structure. Still legal but largely fallen out of favor due to lender complications and the practical limit of 35 investors per property.

Net-leased property. A single tenant under a long-term triple-net lease. Lower management burden than multifamily but concentrated tenant risk.

Qualified Opportunity Zone (QOZ) fund. A different tax-deferral structure (not a 1031 exchange) that can be used with capital gains from any source, not just real estate.

The right choice depends on the investor's tax situation, liquidity needs, risk tolerance, and life stage.

How to Evaluate a DST Sponsor

Because the sponsor controls everything that happens to your investment, sponsor selection is the most important decision in DST due diligence. At a minimum, evaluate:

Years in the DST business and total assets under management

Track record on previous offerings (full-cycle performance, not just current distributions)

Fee structure and alignment of interests (does the sponsor invest its own capital?)

Depth of acquisition, asset management, and investor services teams

Property type focus and underwriting discipline

Transparency of reporting and accessibility of senior leadership

Investors and their CPAs should always review the Private Placement Memorandum (PPM) thoroughly before subscribing.

Common Misconceptions About DSTs

"DSTs are a tax loophole." They aren't. The IRS explicitly blessed the structure in Revenue Ruling 2004-86, and the seven deadly sins exist specifically to keep DSTs within the bounds of Section 1031.

"DSTs are guaranteed." They aren't. Distributions are projected, not promised. The underlying real estate can underperform, and investors can lose principal.

"DSTs are only for high-net-worth investors." Technically yes (accreditation is required), but the minimum investments (often $25,000 to $100,000) are far lower than the equity required to buy comparable property directly.

"A DST is the same as a REIT." It isn't. REITs are publicly traded (in most cases), liquid, and do not qualify as 1031 replacement property. DSTs are private, illiquid, and do qualify.

Frequently Asked Questions

Are DSTs SEC-regulated? Yes. DST offerings are securities, sold under Regulation D exemptions (typically Rule 506(b) or 506(c)) and subject to SEC anti-fraud rules. Sponsors must file Form D with the SEC.

What is the typical hold period for a DST? Most DSTs target a 5-to-10-year hold, with 7 years being common. The actual hold depends on market conditions and the sponsor's exit strategy.

Can I 1031 out of a DST when it sells? Yes. When the sponsor sells the underlying property, investors can elect to roll their proceeds into another 1031 exchange (often into another DST). This is one of the most attractive features of DSTs for long-term tax deferral.

What happens to my DST interest when I die? The DST interest passes to your heirs with a stepped-up cost basis. The deferred capital gain accumulated through prior 1031 exchanges is eliminated for the heirs.

How are DST distributions taxed? Distributions are typically reported on a Form 1099 or K-1 (depending on the structure) and may include a mix of rental income, depreciation pass-through, and return of capital. Most investors find their DST distributions to be largely tax-sheltered in the early years due to depreciation.

What is the minimum DST investment? Minimums vary by sponsor and offering. Common ranges are $25,000 to $100,000 for 1031 exchange investors, and higher (often $250,000 or more) for cash investors who are not coming from an exchange.

The Bottom Line

A Delaware Statutory Trust is a legally recognized, IRS-blessed real estate investment structure that gives 1031 exchange investors access to institutional-grade commercial real estate with no active management responsibility and a clear path to long-term tax deferral. For the right investor (particularly tired landlords, time-pressed exchangers, and those focused on estate planning), DSTs solve real problems.

But DSTs are not a default answer. The seven deadly sins, sponsor risk, illiquidity, and fee structures all warrant careful evaluation before any capital commitment. Investors should work with a qualified CPA, tax attorney, and securities-licensed advisor before subscribing to any DST offering.

Need help thinking through whether a DST fits your 1031 exchange?Talk to a Specialist for a no-obligation conversation about your specific situation, or try our 1031 Calculator to estimate your potential tax deferral.